As of January 8, 2026, Acuity Brands (NYSE: AYI) stands at a pivotal crossroads in its century-long history. Long perceived as a legacy manufacturer of light fixtures and bulbs, the company has spent the last five years aggressively pivoting toward a future defined by the "Internet of Things" (IoT) and intelligent building management. Today’s release of its Fiscal Q1 2026 earnings report serves as a significant proof point for this transformation. With the successful integration of major 2025 acquisitions and a strategic rebranding to Acuity Inc., the company is now positioning itself less as a lighting provider and more as an industrial technology powerhouse. This deep-dive explores how Acuity is navigating a "tepid" traditional construction market while capturing the high-growth wave of the smart-building renaissance.

Historical Background

Acuity’s journey began in 1919 as Atlanta Linen Supply, a humble textile service founded by Isadore Weinstein. The company’s trajectory changed forever in 1969 with the acquisition of Lithonia Lighting, which eventually became the crown jewel of its portfolio. In 2001, Acuity Brands was spun off from National Service Industries (NSI) as an independent public entity.

For decades, Acuity dominated the North American lighting market through scale and a massive distribution network. However, the mid-2010s brought the "LED Revolution," which commoditized the lighting industry and squeezed margins. This forced a radical rethink of the business. The appointment of Neil Ashe as CEO in 2020 marked a definitive shift from "bulbs and ballasts" to "software and sensors." By 2025, the company officially rebranded its corporate umbrella to reflect a focus on intelligent spaces, marking the most significant transformation in its 100-year history.

Business Model

Acuity Brands operates under a dual-segment model that balances stable cash generation with high-growth technology ventures:

- Acuity Brands Lighting and Lighting Controls (ABL): This remains the company’s "cash cow," contributing approximately 78% of total revenue. It encompasses industry-leading brands like Lithonia Lighting, Holophane, and Peerless. ABL focuses on high-volume manufacturing of architectural and commercial lighting, using its "Acuity Business System" (ABS) to maintain industry-leading margins through operational efficiency.

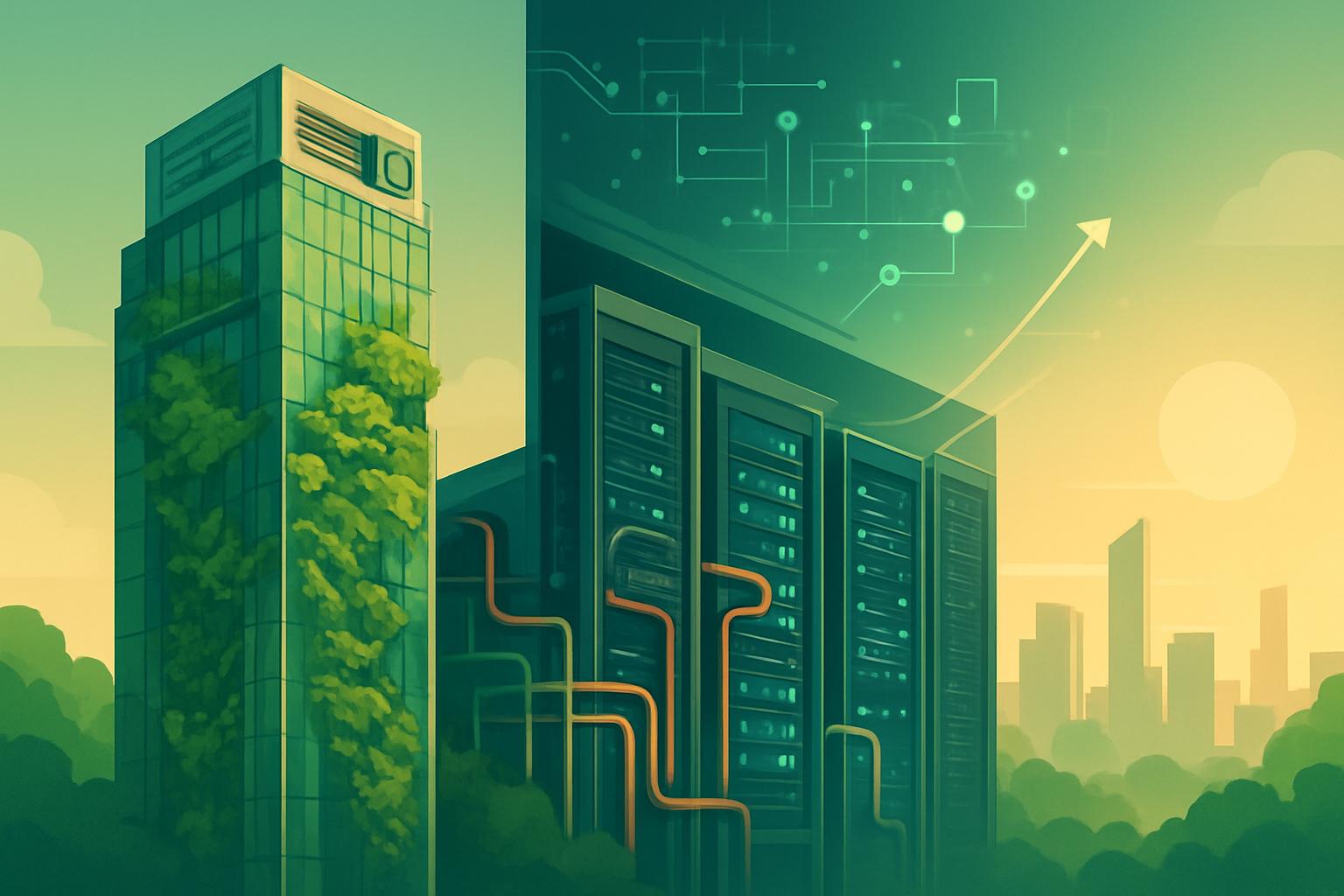

- Acuity Intelligent Spaces (AIS): This is the high-growth "tech" engine of the company. It includes Distech Controls (building automation), Atrius (sustainability software), and the newly acquired QSC (audio, video, and control platforms). AIS focuses on the "brain" of the building—managing HVAC, lighting, and audio systems through a unified software stack to optimize energy use and user experience.

Stock Performance Overview

Over the past decade, AYI has been a story of a "U-shaped" recovery.

- 10-Year View: The stock faced significant headwinds between 2016 and 2020 as the LED transition reached saturation.

- 5-Year View: Since the 2020 management change, the stock has outperformed the broader industrial sector, rising from roughly $90 to today’s levels near $380.

- 1-Year View: The last 12 months have been particularly robust, with the stock rallying nearly 40% as investors rewarded the company’s expansion into software-defined building management. Today, the stock trades at an all-time high, reflecting a market that is finally applying a "tech multiple" to a once-stodgy industrial name.

Financial Performance

Acuity’s Q1 2026 earnings, reported today (1/8/2026), highlight a company successfully managing a transition:

- Revenue: Reported at $1.14 billion, a 20.2% year-over-year increase, largely fueled by the inorganic growth of the Intelligent Spaces segment.

- Profitability: Adjusted EPS hit $4.69, beating analyst expectations. Adjusted operating margins expanded to 17.2%, an impressive feat given the inflationary pressures in the global supply chain.

- Segment Strength: While the ABL lighting segment saw a modest 1% organic growth, the AIS segment revenue surged 250% (inclusive of the QSC acquisition).

- Balance Sheet: Acuity maintains a conservative leverage profile with a debt-to-equity ratio of approximately 0.37, providing ample "dry powder" for further M&A in the software space.

Leadership and Management

CEO Neil Ashe is widely credited with the "Acuity 2.0" strategy. A former executive at Walmart and CBS Interactive, Ashe brought a "digital-first" mindset to a manufacturing culture. His signature initiative, the Acuity Business System (ABS), is a lean management framework designed to drive "product vitality"—a metric tracking the percentage of revenue derived from products launched in the last three years. This focus on constant innovation has allowed Acuity to maintain pricing power even in a competitive lighting market. The leadership team is viewed by Wall Street as disciplined capital allocators, favoring share repurchases and strategic, bolt-on technology acquisitions over high-risk, dilutive mega-mergers.

Products, Services, and Innovations

Innovation at Acuity is now centered on the "Interoperable Building." Key products include:

- Distech Controls’ ECLYPSE Apex: A powerful edge controller that allows buildings to run autonomous HVAC and lighting routines using AI.

- QSC Q-SYS Platform: Following the 2025 acquisition, this platform integrates audio and video data with building controls, allowing a facility manager to see not just if lights are on, but how a space is being used through voice and vision sensors.

- Atrius Sustainability: A cloud-based platform that helps Fortune 500 companies track their carbon footprint in real-time, directly responding to new global ESG reporting mandates.

Competitive Landscape

Acuity competes on two fronts, which presents a unique challenge:

- In Lighting: It faces Signify (AMS: LIGHT), Hubbell (NYSE: HUBB), and Cooper Lighting. Acuity differentiates here through its superior North American distribution network and its ability to bundle lighting with proprietary controls.

- In Building Management: It squares off against giants like Honeywell (NASDAQ: HON), Johnson Controls (NYSE: JCI), and Schneider Electric. While these competitors are much larger, Acuity’s "agnostic" software approach—allowing its tools to work with third-party hardware—gives it a "nimble tech" advantage.

Industry and Market Trends

The "Smart Building Renaissance" is the primary tailwind for 2026. Global energy costs and aging infrastructure are forcing commercial real estate owners to retrofit buildings for efficiency. Furthermore, the "flight to quality" in office spaces means landlords are investing in high-end AV and atmospheric lighting to lure workers back to the office. The integration of AI into building controllers—allowing for "predictive maintenance"—is the next major frontier that Acuity is currently spearheading.

Risks and Challenges

Despite its strong performance, Acuity is not without risks:

- Cyclicality: The commercial construction market is sensitive to interest rates. A "higher-for-longer" rate environment could delay new projects, impacting the ABL segment.

- Integration Risk: The $1.2 billion QSC acquisition is the largest in company history. Any cultural or technical friction in integrating this AV platform could stall AIS growth.

- Commoditization: Low-cost LED imports from overseas continue to put pressure on the lower-end "contractor" grades of lighting fixtures.

Opportunities and Catalysts

- The Inflation Reduction Act (IRA): Continued government incentives for energy-efficient building upgrades provide a multi-year tailwind for Distech and Atrius products.

- Data Monetization: As Acuity collects more data on building usage, there is a significant opportunity to transition toward a "Software-as-a-Service" (SaaS) model with recurring monthly revenue.

- International Expansion: While dominant in North America, Acuity has significant room to grow its AIS footprint in European and Asian markets.

Investor Sentiment and Analyst Coverage

Wall Street sentiment has shifted from "Neutral" to "Moderate Buy" over the last 18 months. Analysts are increasingly viewing AYI as a way to play the "AI in physical spaces" theme without the volatility of pure-play tech stocks. Hedge fund ownership increased in late 2025, signaling institutional confidence in the QSC acquisition. However, some value-oriented analysts caution that the current P/E of 29x leaves little room for error in execution.

Regulatory, Policy, and Geopolitical Factors

New SEC climate disclosure rules (and similar mandates in the EU) are a massive indirect catalyst for Acuity. Since buildings account for nearly 40% of global carbon emissions, corporations must use tools like Atrius to accurately report and reduce their energy consumption. Geopolitically, Acuity’s focus on "on-shoring" and its significant North American manufacturing footprint insulate it somewhat from the escalating trade tensions and tariffs affecting competitors who rely heavily on Chinese manufacturing.

Conclusion

Acuity Brands (now Acuity Inc.) has successfully navigated the difficult transition from a hardware manufacturer to an industrial technology leader. Today’s Q1 2026 results confirm that while the legacy lighting business provides the essential floor of cash flow, the Intelligent Spaces Group is providing the ceiling for growth. For investors, the key will be monitoring whether the company can maintain its high software margins as it scales. As the world moves toward autonomous, carbon-neutral buildings, Acuity is no longer just lighting the room—it’s providing the intelligence that runs the building.

This content is intended for informational purposes only and is not financial advice.