As the first month of 2026 reaches its crescendo, a high-stakes financial battle is playing out not just on the trading floors of Wall Street, but in the digital arenas of prediction markets. On Polymarket, the world’s largest decentralized prediction platform, a market titled "Largest Company by Market Cap at end of January?" has surpassed $10 million in trading volume. Traders are putting millions on the line to forecast whether Nvidia (NASDAQ: NVDA) can maintain its status as the world’s most valuable company through the end of the month.

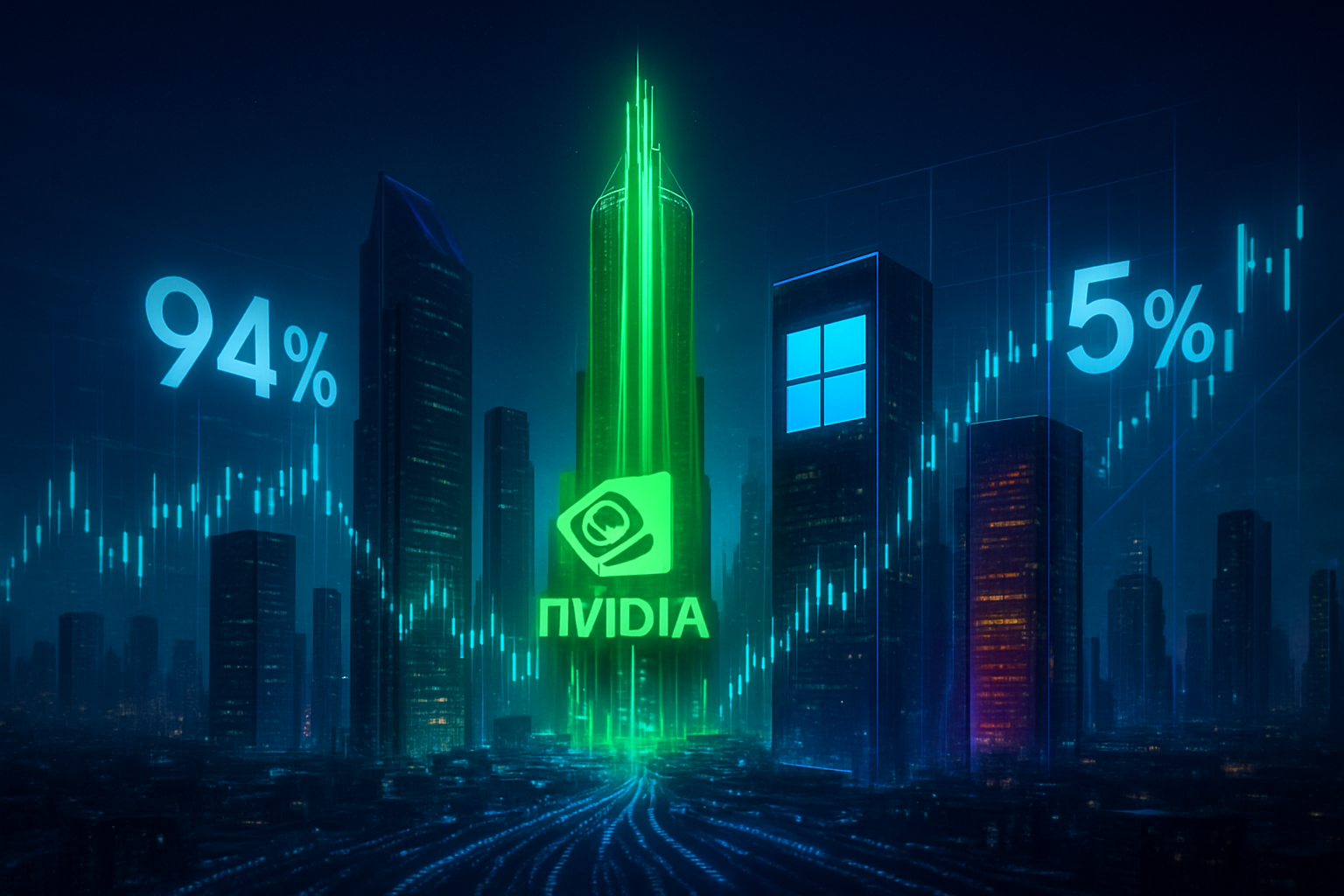

Currently, the odds are heavily skewed in favor of the semiconductor giant, with "Yes" shares for Nvidia trading at roughly 94 cents—implying a 94% probability of dominance. Despite the commanding lead, the market has seen a flurry of activity as competitors like Alphabet Inc. (NASDAQ: GOOGL) surge in value, creating a rare window of volatility that has captured the attention of both retail speculators and institutional hedgers.

The Market: What's Being Predicted

The specific market on Polymarket asks a straightforward but high-consequence question: Which company will have the highest market capitalization as of the close of business on January 31, 2026? While the contract includes options for perennial heavyweights like Apple Inc. (NASDAQ: AAPL) and Microsoft Corp. (NASDAQ: MSFT), the primary action is centered on Nvidia’s ability to defend its title.

As of January 19, 2026, the market caps stand in a hierarchy that would have seemed unthinkable just two years ago:

- Nvidia (NVDA): ~$4.55 Trillion (94% odds)

- Alphabet (GOOGL): ~$4.02 Trillion (5% odds)

- Apple (AAPL): ~$3.79 Trillion (<1% odds)

- Microsoft (MSFT): ~$3.42 Trillion (<1% odds)

The liquidity in this market is exceptionally high for a short-term corporate event, with over $10.2 million in total volume. Resolution is tied to verified closing data from major financial aggregators, such as CompaniesMarketCap or Bloomberg. The market has seen significant shifts over the last two weeks; earlier in January, Alphabet’s odds were virtually non-existent, but a sudden rally sparked by a landmark AI integration deal saw "Yes" shares for Google’s parent company spike briefly to 15% before settling.

Why Traders Are Betting

The primary driver for the current betting frenzy is the stark contrast between Nvidia’s stable trajectory and the upcoming "Magnificent Seven" earnings gauntlet. Analysts from firms like Wolfe Research remain aggressively bullish on Nvidia, citing the transition to the "Rubin" chip architecture as a catalyst that could push the stock toward a $6 trillion valuation by late 2026. However, prediction market traders are focused on a much tighter window.

The "whale" activity in this market suggests a sophisticated hedging strategy. Because Nvidia is not scheduled to report its own earnings until February 25, 2026, its market cap is perceived as less susceptible to a sudden idiosyncratic crash in the next 12 days. Conversely, Microsoft and Apple are both slated to report earnings on January 28 and January 29, respectively.

"Traders are essentially betting on the 'earnings gap,'" says one high-volume Polymarket participant. "If Microsoft or Apple were to report a massive beat, they could theoretically close a $500 billion gap in a single session. But at a 94% probability, the market is signaling that Nvidia’s $700 billion lead over Apple is an insurmountable 'moat' for the month of January."

Broader Context and Implications

This $10 million market is a microcosm of a larger trend: the "financialization" of market sentiment. Traditional analyst predictions often focus on 12-month price targets and fundamental ratios, which can be slow to react to daily momentum. Prediction markets, however, provide a real-time "probability scoreboard" that incorporates macro risks, technical levels, and even geopolitical rumors.

The rise of Alphabet to the #2 spot, overtaking Apple earlier this month, was reflected in Polymarket odds hours before many traditional brokerages updated their morning notes. This reveals a "wisdom of the crowd" effect where prediction markets act as a leading indicator for sentiment shifts among tech investors.

Furthermore, the focus on "Market Cap King" status has real-world implications for passive investment flows. When a company holds the #1 spot, it often commands a larger weight in S&P 500 and Nasdaq-100 indices, forcing institutional buying. Polymarket traders are, in effect, betting on the direction of these massive, automated capital flows.

What to Watch Next

The next 12 days will be critical for the resolution of this market. While Nvidia holds a massive lead, two specific events could flip the odds:

- January 28 – Microsoft Earnings: If Microsoft reports a breakthrough in Azure AI margins that triggers a 15-20% rally, the gap between it and Nvidia could shrink overnight, though it currently remains the "dark horse" of the group.

- January 29 – Apple Earnings: As the former #1, Apple has the most historical volatility around its earnings reports. A "monster" quarter fueled by AI-integrated iPhone sales could see it leapfrog Alphabet and challenge Nvidia.

However, the most likely scenario remains a "Nvidia Walkover." With no earnings report to act as a negative catalyst, Nvidia would likely only lose its top spot if a broader macro-economic shock hit the semiconductor sector specifically—a scenario that currently has low probability according to broader options market data.

Bottom Line

The $10 million Polymarket battle over the world’s largest company highlights a shift in how we measure corporate success. While analysts are debating where Nvidia will be in 2027, prediction market traders are ruthlessly calculating the probability of its dominance over the next 288 hours.

The current 94% odds for Nvidia suggest that the "AI King" is safe for now, but the 5-6% odds for Alphabet represent a "non-zero" chance that the recent shuffling in the tech hierarchy isn't over. For investors, these markets offer a unique window into the "tail risks" that traditional research might overlook. As the month draws to a close, all eyes will be on whether the semiconductor giant can hold its $4.5 trillion throne against the impending earnings-season volatility.

This article is for informational purposes only and does not constitute financial or betting advice. Prediction market participation may be subject to legal restrictions in your jurisdiction.

PredictStreet focuses on covering the latest developments in prediction markets.

Visit the PredictStreet website at https://www.predictstreet.ai/.